# ================================================================

# Case Study 6 — Historical shape (ggplot2) + OC curves (base R)

# - One-sided sampling (Ac = 0), uniform axes across OC figures

# - Legend with AQL / LTPD / LQ20 values included

# - Four separate OC plots: n = 32, 50, 80, 125

# ================================================================

suppressPackageStartupMessages(library(ggplot2))

set.seed(123)

# -----------------------------

# 0) Setup (one-sided LSL case)

# -----------------------------

LSL <- 98.0

U <- 102.0 # only for the illustrative historical distribution

# A left-skewed Beta(alpha, beta) on [LSL, U] when alpha > beta:

alpha_hat <- 8

beta_hat <- 2.6

# Generator for the illustrative “historical” data:

# by construction, ALL values are >= LSL (no OOS).

r_hist <- function(n) LSL + (U - LSL) * rbeta(n, alpha_hat, beta_hat)

# -----------------------------

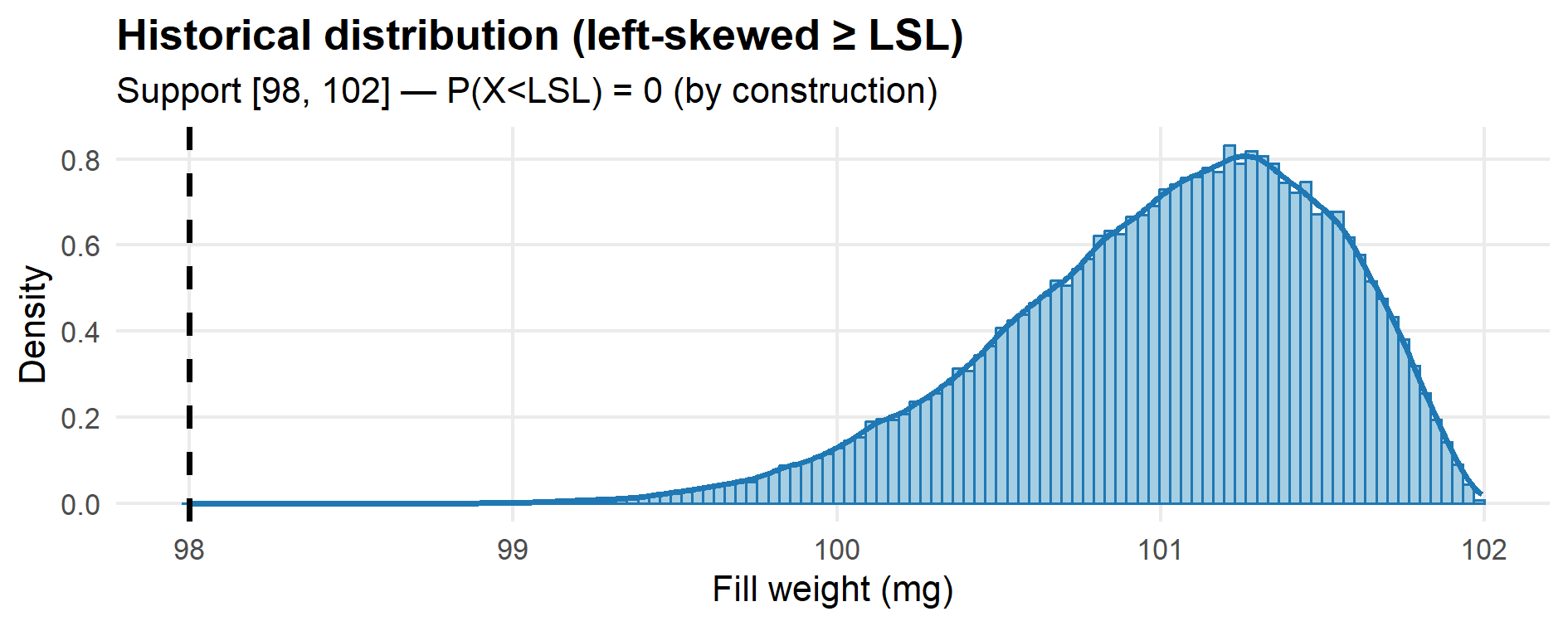

# 1) Historical distribution

# -----------------------------

hist_x <- r_hist(100000)

stopifnot(all(hist_x >= LSL)) # defensive check

p_hist <- ggplot(data.frame(x = hist_x), aes(x)) +

geom_histogram(aes(y = after_stat(density)),

bins = 120, fill = "#a6cee3", color = "#1f78b4") +

geom_density(linewidth = 1.1, color = "#1f78b4") +

geom_vline(xintercept = LSL, linetype = 2, linewidth = 1) +

labs(title = "Historical distribution (left-skewed ≥ LSL)",

subtitle = sprintf("Support [%g, %g] — P(X<LSL) = 0 (by construction)", LSL, U),

x = "Fill weight (mg)", y = "Density") +

theme_minimal(base_size = 13) +

theme(plot.title = element_text(face = "bold"),

panel.grid.minor = element_blank())

print(p_hist)

# ggsave("fig12_1_historical.png", p_hist, width = 10, height = 3.6, dpi = 150)

# -------------------------------------

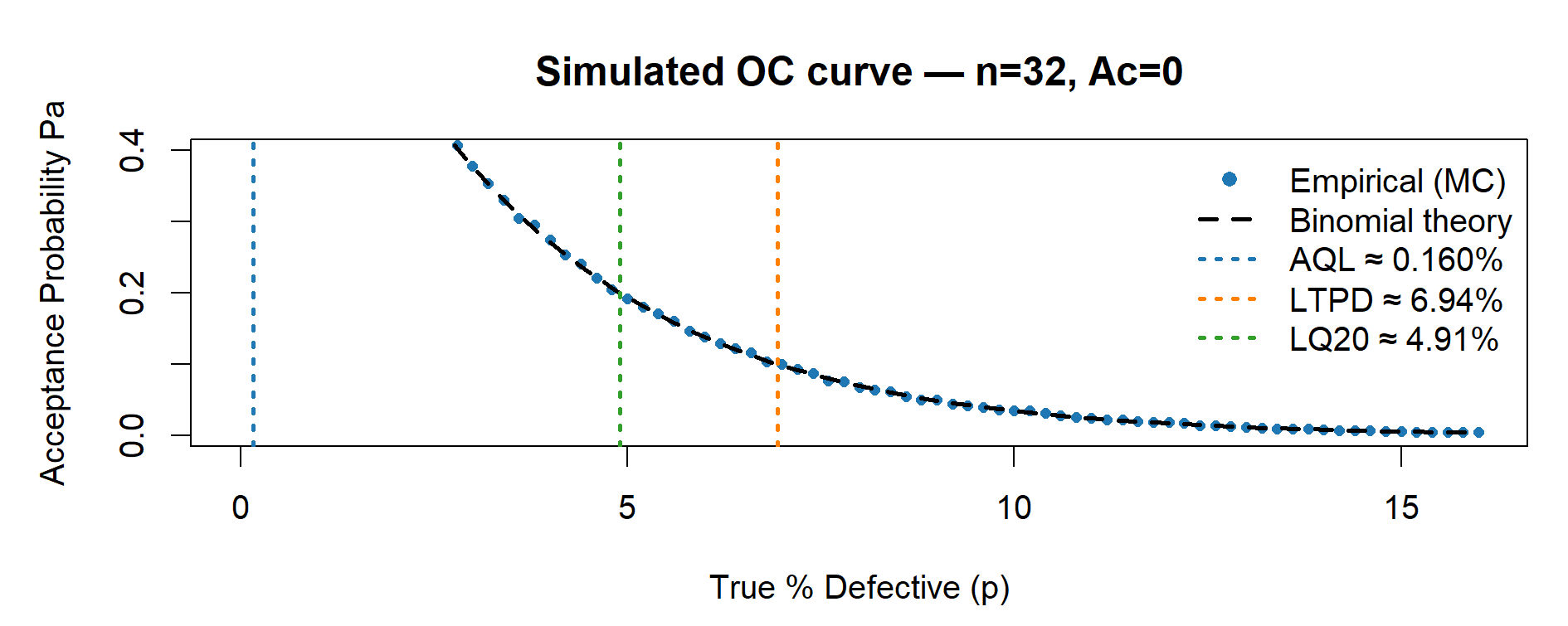

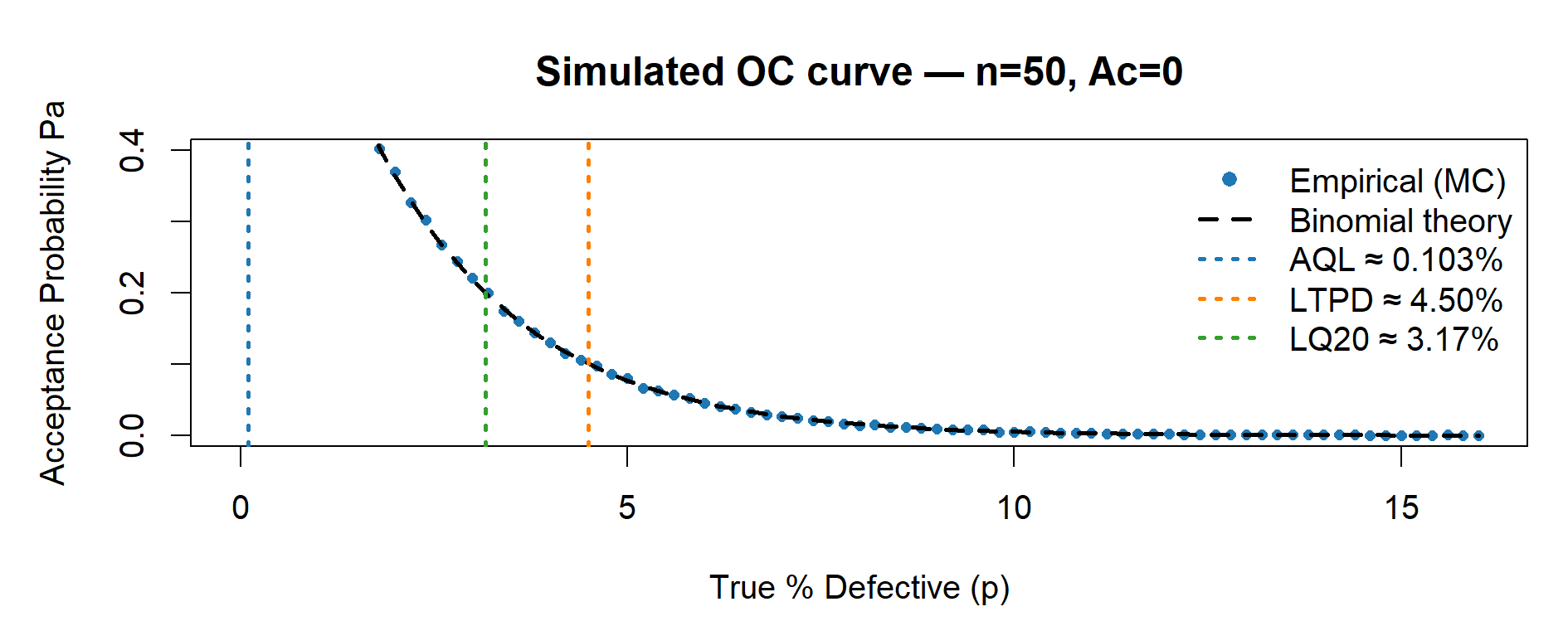

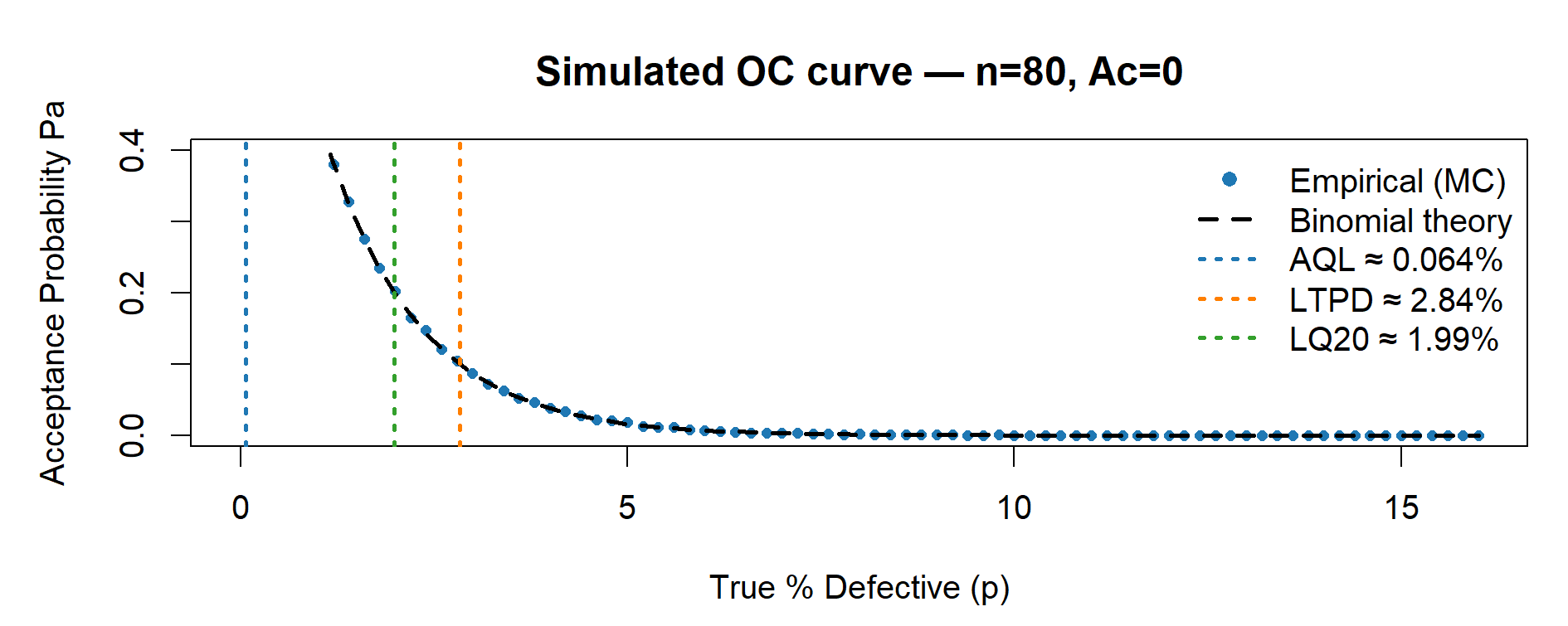

# 2) OC settings and helper functions

# -------------------------------------

# Uniform axes across all OC plots (for visual comparability)

xlim_percent <- c(0, 16) # x: 0–16% defectives

ylim_common <- c(0, 0.40) # y: Pa 0.00–0.40

# Grid of true defect rates p (in fraction). We will plot in percent.

p_grid <- seq(0, xlim_percent[2] / 100, by = 0.002)

# Monte Carlo reps for empirical Pa; increase if you want smoother dots

reps <- 20000

# Empirical acceptance probability at a given p

Pa_empirical <- function(n, Ac, p, reps = 20000) {

# For Ac = 0, accept if K = 0 with K ~ Bin(n, p).

mean(rbinom(reps, size = n, prob = p) <= Ac)

}

# One OC figure (base R): empirical (points) + binomial theory (dashed line)

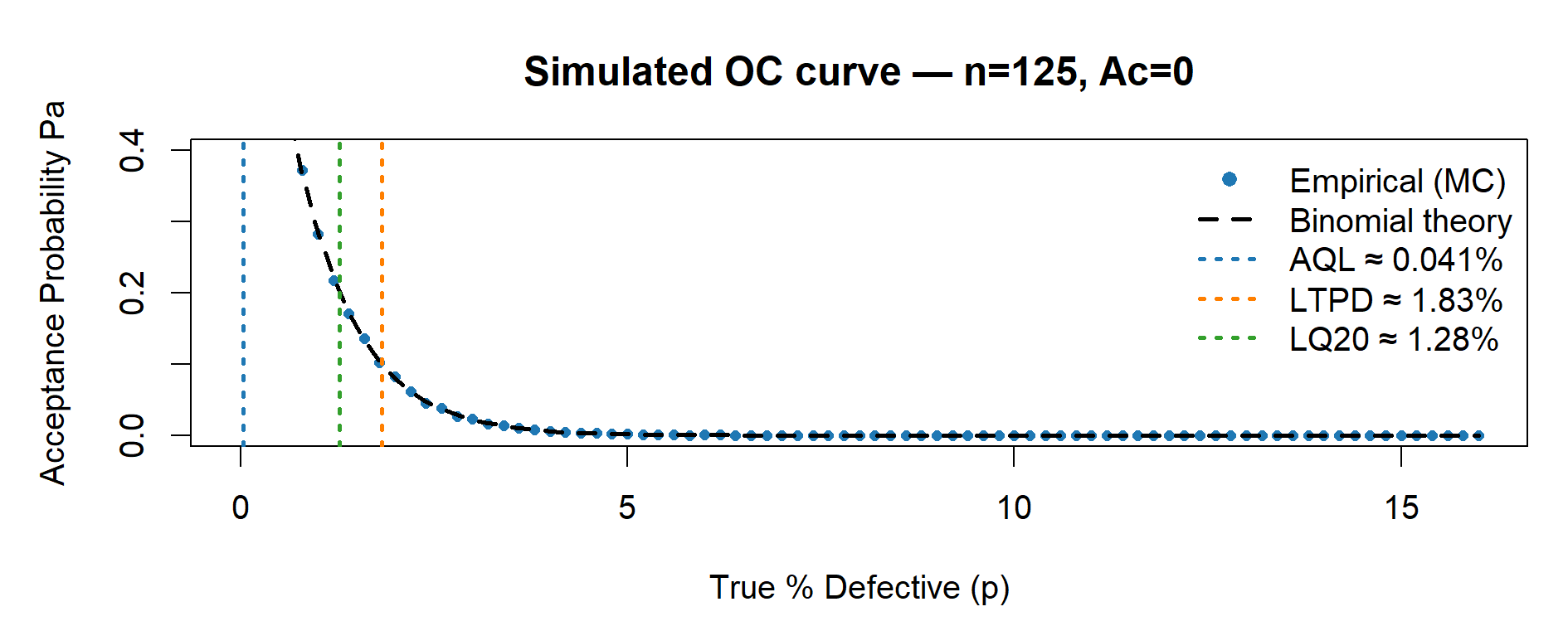

plot_OC_base <- function(n, Ac = 0L) {

# Curves

Pa_emp <- sapply(p_grid, function(p) Pa_empirical(n, Ac, p, reps))

Pa_the <- pbinom(Ac, n, p_grid) # For Ac=0, equals (1 - p)^n

# Risk points (closed form for Ac = 0)

p_AQL <- 1 - 0.95^(1 / n) # Pa ~ 0.95

p_LTPD <- 1 - 0.10^(1 / n) # Pa ~ 0.10

p_LQ20 <- 1 - 0.20^(1 / n) # Pa ~ 0.20

# Plot

par(mar = c(4.5, 4.8, 3.5, 1))

plot(p_grid * 100, Pa_emp,

type = "p", pch = 16, cex = 0.7, col = "#1f78b4",

xlim = xlim_percent, ylim = ylim_common,

xlab = "True % Defective (p)", ylab = "Acceptance Probability Pa",

main = sprintf("Simulated OC curve — n=%d, Ac=%d", n, Ac))

lines(p_grid * 100, Pa_the, lty = 2, lwd = 2, col = "#000000") # Binomial theory

# Vertical markers (thicker, color-coded)

abline(v = 100 * p_AQL, lty = 3, lwd = 2, col = "#1f78b4") # AQL (blue)

abline(v = 100 * p_LTPD, lty = 3, lwd = 2, col = "#ff7f00") # LTPD (orange)

abline(v = 100 * p_LQ20, lty = 3, lwd = 2, col = "#33a02c") # LQ20 (green)

# Single legend with numeric values

legend("topright",

legend = c("Empirical (MC)",

"Binomial theory",

sprintf("AQL \u2248 %.3f%%", 100 * p_AQL),

sprintf("LTPD \u2248 %.2f%%", 100 * p_LTPD),

sprintf("LQ20 \u2248 %.2f%%", 100 * p_LQ20)),

col = c("#1f78b4", "#000000", "#1f78b4", "#ff7f00", "#33a02c"),

pch = c(16, NA, NA, NA, NA),

lty = c(NA, 2, 3, 3, 3),

lwd = c(NA, 2, 2, 2, 2),

pt.cex = 1.0,

bty = "n")

# Return the three key percentages (for tables)

invisible(c(AQL = 100 * p_AQL, LTPD = 100 * p_LTPD, LQ20 = 100 * p_LQ20))

}

# --------------------------------------

# 3) Four separate OC plots (not a panel)

# --------------------------------------

risk_n32 <- plot_OC_base(32, Ac = 0L)

risk_n50 <- plot_OC_base(50, Ac = 0L)

risk_n80 <- plot_OC_base(80, Ac = 0L)

risk_n125 <- plot_OC_base(125, Ac = 0L)

# Optional PNG export:

# png("fig12_2_OC_n32.png", 1400, 500, res = 130); plot_OC_base(32); dev.off()

# png("fig12_3_OC_n50.png", 1400, 500, res = 130); plot_OC_base(50); dev.off()

# png("fig12_4_OC_n80.png", 1400, 500, res = 130); plot_OC_base(80); dev.off()

# png("fig12_5_OC_n125.png",1400, 500, res = 130); plot_OC_base(125); dev.off()

# --------------------------------------

# 4) Summary tables (percent + counts/1e6)

# --------------------------------------

# First, assemble a compact table with AQL, LTPD, LQ20 by plan:

risk_table <- rbind(

`n=32, Ac=0` = round(risk_n32, 3),

`n=50, Ac=0` = round(risk_n50, 3),

`n=80, Ac=0` = round(risk_n80, 3),

`n=125, Ac=0` = round(risk_n125, 3)

)

# Then build a data.frame with “clean” column names (no spaces)

risk_df <- data.frame(

Plan = rownames(risk_table),

AQL_pct = risk_table[, "AQL"],

LTPD_pct = risk_table[, "LTPD"],

LQ20_pct = risk_table[, "LQ20"]

)

# Counts per 1,000,000 units (helps with interpretability on slides)

risk_df$AQL_cnt_1e6 <- round(risk_df$AQL_pct / 100 * 1e6)

risk_df$LTPD_cnt_1e6 <- round(risk_df$LTPD_pct / 100 * 1e6)

risk_df$LQ20_cnt_1e6 <- round(risk_df$LQ20_pct / 100 * 1e6)

print(risk_df, row.names = FALSE)